In the last five years, the payments landscape in India has gone through significant changes. India has graduated from being a cash-dominated economy to a digital economy.

All the modes of digital payments in India have shown steady growth. In the more recent years, UPI has been in the news for unheard of growth every month. In October, the total value of transactions over UPI crossed the $100 billion mark.

While UPI is being celebrated currently for being the flag bearer of digital payments in India, let’s not forget about the time-tested payments systems that have been slowly taking the country on the digital path.

This has been possible only because of the continuous efforts of India’s apex bank, the Reserve Bank of India. It brought out several digital payments instruments suited for different use cases.

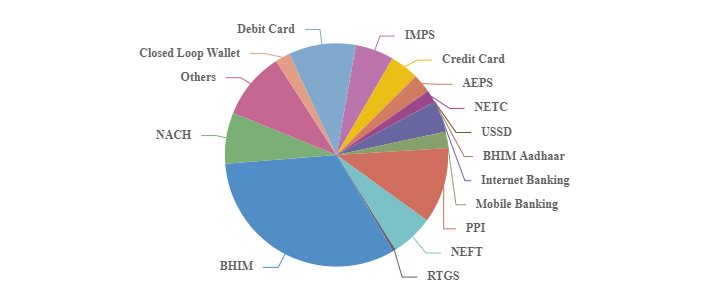

Different digital payment instruments

Let’s briefly look at the three ways through which one can do net banking in India:

- NEFT: National Electronics Funds Transfer is a centralised payment system started and operated by RBI. NEFT is available throughout the year and works even during non-banking hours

- RTGS: Real-time Gross Settlements is a payments rail made for large-ticket funds transfer. The specialty of RTGS is that the settlements happen on an individual basis, and thus are quicker than NEFT

- IMPS: Immediate Payment System is operated by the National Payments Council of India (NPCI). It is made for low-value transactions, which are largely used for retail consumers. It can be used 24×7 throughout the year. But one can transfer only Rs 5 lakh per transaction and Rs 20 lakh a day via IMPS

What is RTGS?

Launched in March 2004, RTGS or Real-Time Gross Settlement is the oldest payments mode in India.

Unlike other payment methods, fund settlements over RTGS payments rail happen in the books of RBI. It doesn’t require the central bank to net debits with credits and then process the payments. This makes it instant and efficient.

Real-time refers to the processing of payments instructions as soon as they are received. Gross settlement points out the fact that the settlement process is on an individual order basis.

It is to be noted that RTGS funds transfer is final and irrevocable.

Is there a limit on RTGS funds transfer?

While technically, there are no limitations to how much money can be transferred via RTGS, individual banks have put different caps on transfers.

For example, ICICI Bank, HDFC Bank, and a few others allow their customers to use RTGS only if they transfer a minimum of Rs 2 lakh. While HDFC has capped the higher limit of transactions on RTGS to Rs 10 lakh per day, ICICI has capped the daily limit to Rs 20 lakh. On the other hand, the State Bank of India doesn’t put any limit on the maximum amount one can transfer, as long as the minimum transfer amount is Rs 2 lakh.

It’s better to first check with your bank about the minimum and maximum amount one can transfer using RTGS.

Do RTGS payments levy transaction charges?

Online RTGS transactions don’t levy any charges. However, if one were to make RTGS payments by physically going to a bank branch, there is a nominal transaction charge. RBI has capped transaction charges at Rs 49.50 for sending Rs 2 lakh to 5 lakh. For amounts exceeding Rs 5 lakh, the transaction charge is capped at Rs 49.50.

RBI allows banks to charge users less than these, but they can’t levy a higher rate than stipulated by the RBI.

How and when to transfer funds through RTGS

Making a payment through RTGS is quite simple and fast.

You just need to log in to your bank’s account and go to the fund transfer of payments page. There, choose RTGS as the mode of payment. If the payee’s account is not already added to your account, you will have to first put in their bank account details such as account number, name, and IFSC.

Once these details are added you can proceed to make the payment by choosing RTGS from the list of other payment methods.

RTGS payments can happen only if both the payer and receiver’s bank branches are RTGS enabled. There are more than 1.65 lakh bank branches that can process RTGS payments. You can find the list of banks that are eligible for this here.

You should transfer money via RTGS if:

- The amount to be transferred is equal to or more than Rs 2 lakh

- You want to ensure the payee receives the money instantly. RTGS remittances take a maximum of 30 minutes. Last year in December, RBI made RTGS transfers available 24×7, which can be used 365 days

- You don’t want to visit a bank branch for a large funds transfer

Benefits of using RTGS

- It is a safe and secure system for funds transfer

- RTGS transactions/transfers have no amount cap

- It’s real-time and is available throughout the year, irrespective of holidays

- There is no need to issue a physical cheque or generate a demand draft

- Electronic transfer of money makes it convenient to use

- Transaction charges have been capped by RBI

Benefits of RTGS over other payment methods for businesses

The ease of doing business depends on a lot of factors, and one among them is the flexibility and freedom of payments infrastructure a country provides.

Since RBI has made RTGS payments available throughout the year and round the clock, it is set to improve India’s chances of ease of doing business. It was also done to increase the digitization of payments.

RTGS is specifically useful for businesses as it deals with high ticket money transfers, which is a typical and frequent use case for businesses. Moreover, it also solves the immediacy issue as the settlements happen in real-time, which takes a maximum of 30 minutes.

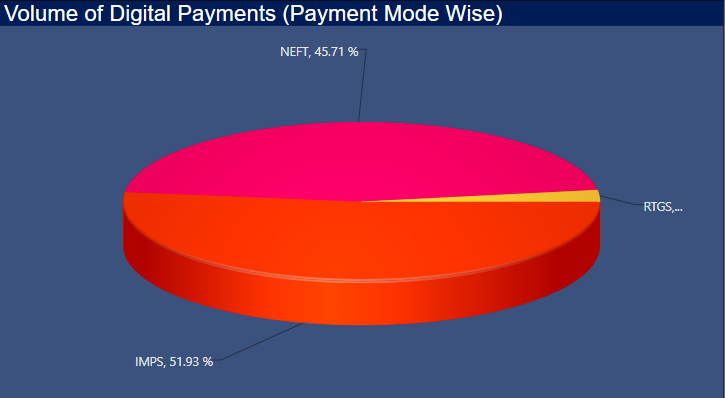

This is in stark contrast with NEFT funds transfer, a close cousin of RTGS payments. Similar to RTGS, payments made through NEFT are also high-ticket. But the RTGS payments system gets an extra star for settling payments in real-time. NEFT payments are settled in batches instead of on an individual basis, which makes it longer for the payee to receive the money.

Paytm Payment Gateway makes digital payments easy

For an overall digital payments solution, you may want to sign up for Paytm Payment Gateway. From one dashboard, you can manage payments using different payment systems.

Paytm Payment Gateway is ideal for your business if you want to:

- Receive payments from customers without delay

- Enable your business to receive payments from global clients

- Manage refunds

- Run a subscription business

- Get detailed business analytics

If you are looking for any of these solutions, sign up for Paytm Payment Gateway right now and see how it does wonders for your business.