“Look at what India has accomplished with the UPI, Aadhaar, and the payments stack, and you will see the value of having an open, connected stack which works. And that is what the internet is. Having responsible regulation which preserves all of this are some of the core elements.”

These are the thoughts of Sundar Pichai, CEO of Google and Alphabet, on the various Indian initiatives in digitising and adopting technology to modernise something as simple as daily payments.

The Unprecedented Growth of UPI

During the pandemic year 2020-21, UPI experienced phenomenal growth, and several countries have expressed an interest in learning from the Indian observation to replicate the model. COVID-19 encouraged the Indian public to use online methods for financial transactions, and UPI growth was phenomenal during the pandemic.

During the coronavirus pandemic that gripped the entire world in 2020-21, upwards of 22 crore UPI transactions valued at Rs 41 lakh crore were recorded.

The adoption rate of UPI among the Indian public is rising. It is driving the overall adoption of digital transactions in the country. The graph below highlights the year-on-year growth of UPI transactions since inception:

UPI transaction volumes continue to grow

Source: NPCI

Source: NPCI

The UPI transaction volumes in March 2021 closed at 2,732 million, 119% more than the previous year. The transaction volume saw unprecedented growth and closed at 5,406 million, 98% more than the year before.

As of November 2022, the transaction volume has increased by 35% to 7,309 million from March 2022.

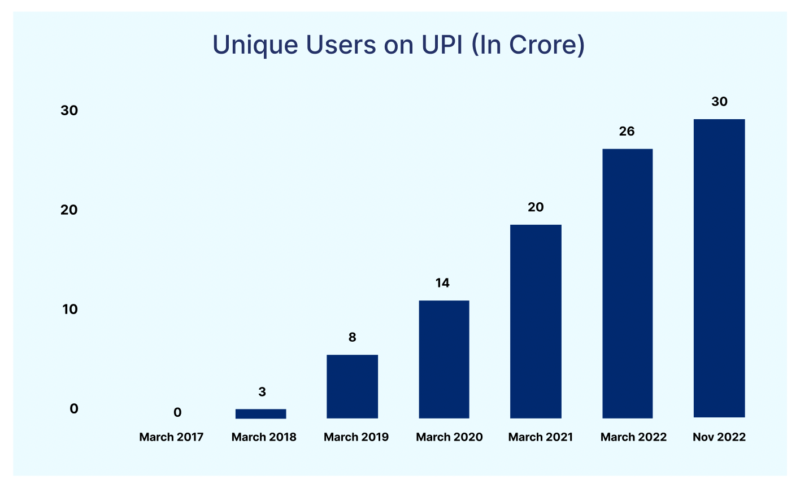

Here’s another graph that highlights the growth of active UPI users.

The database of unique UPI users continues to grow

Source: GoI Report

Source: GoI Report

The number of active users on UPI in March 2021 closed at 14 crores which were 43% more than the number of users in March 2020. The user base saw 30% and closed at 26 crores in March 2022.

As of November 2022, the number of active UPI users has increased by 15% to 30 crores from March 2022.

India Tops in the Adoption of Digital Transactions Globally

According to ACI Worldwide, India reported the most real-time transactions (48 billion) last year. As per the report, India surpassed its neighbour China, which recorded 18 billion real-time transactions, 6.5 times more than the transactions recorded by the US, UK, Germany, Canada, and France combined.

Source: ACI Worldwide

Source: ACI Worldwide

It could be attributed to merchants’ increasing adoption and use of UPI-based QR code payments and mobile payment apps. The increase was also due to the increased adoption of digital payments during the pandemic, which contributed to India’s real-time payments capturing 31% of the total payments transaction volume last year.

Furthermore, India’s share of real-time payments in the total global payments volume is projected to reach 70% by 2026, with the combined net savings for consumers and businesses reaching $92.4 billion.

Definition of Real-Time Payments (RTP)

Real-Time Payment (RTP) refers to any account-to-account transfer of funds that enables the instant availability of funds to the transaction’s beneficiary.

Real-time payments provide proof of fund transfer through a real-time balance; once payment is authorised, the payer’s account immediately reflects the deduction of funds.

Though settlement times vary from scheme to scheme, it usually takes only a couple of seconds. Hence, real-time payments are often known as instant payments.

Also Read: How India Paid in 2022: An Annual Overview of Digital Payments

Various Nations to Replicate India’s Digital Revolution via UPI

These encouraging statistics on UPI have surprised the world so much that many developed and developing nations are considering replicating it.

UPI in Nepal

At the beginning of this year, NPCI International Payments (NIPL), the global arm of NPCI, announced that it will assist Nepal in implementing the platform.

NIPL has collaborated with Gateway Payments Service (GPS), a Nepal-based authorised payment system operator, and Bengaluru-based Manam Infotech.

UPI will be used in Nepal as a digital public benefit to improve real-time interoperable person-to-person (P2P) and merchant-to-merchant (P2M) payment transactions.

As a payments platform, UPI will facilitate an open interoperable system for real-time payments in Nepal, as well as financial inclusion. It will also lay the groundwork for cross-border P2P remittances between Nepal and India in real-time.

UPI will allow the final segment of Nepalese consumers to reap the benefits of an open, interoperable payment system. UPI will help catalyse the process of achieving financial inclusion in Nepal and reshape the regional economy by opening new opportunities.

It will contribute to the modernisation of Nepal’s digital payment infrastructure and introduce the convenience that digital payments offer to the citizens of Nepal.

Recognition from Google in the US

In late 2019, Google wrote a letter to the US Federal Reserve suggesting they replicate India’s UPI model for its proposed interbank real-time gross settlement (RTGS) service.

During the exchanges, Google also discussed the experience of launching its payments app that uses the technology in India. The app was launched in collaboration with regulatory authorities and the payments ecosystem.

The collaboration further aided in driving and scaling UPI usage via Google’s payment app, which now has more than 150 million monthly active users in India.

Where’s UPI headed globally?

IT Minister Ashwini Vaishnaw earlier this year stated during Digital India Week that India is in talks with 30 countries about UPI and that three countries have already signed memorandums of understanding (MoUs) in this regard.

In addition to Nepal, NPCI International has previously collaborated with institutions in the UAE, Singapore, Japan, and China. NPCI will now work on establishing this payment techhnology as a channel for cross-border remittances.

NPCI International also entered into an MoU with Lyra Network of France in June 2022 to enable accepting UPI and RuPay Cards in the country.

Also Read: UPI, RuPay to Go Global, in Talks with Foreign Countries to Make It Acceptable

Factors Contributing to the Continued Growth of UPI in India

UPI is the backbone of the ongoing financial revolution. Before 2016, nobody would have predicted that a cash-based economy like India would experience a massive surge in digital payments.

Whether it is a tea seller selling a Rs 10 Cutting Chai or a showroom selling expensive products, a significant section of Indian society has adopted UPI for daily operations.

Highlighted below are the key macro factors driving UPI growth:

Internet penetration

India has 692 million active internet users, with 351 million in rural India and 341 in urban India. According to a report by The Internet and Mobile Association of India, the country will have 900 million internet users by 2025.

Government schemes such as PM-WANI and BharatNet, as well as Jio’s internet revolution, have provided citizens with high-speed internet at the lowest possible cost.

It is estimated that approximately 346 million Indians participate in digital transactions such as online payments and e-commerce.

Availability of cheap smartphones

Easy access to smartphones was a roadblock a decade ago. However, the disruption in the smartphone segment over recent years resulted in 492.78 million smartphone users by 2021, as per Statista.

According to Deloitte, India will have one billion smartphone users by 2026, primarily driven by smartphone sales in rural areas.

In March 2022, the RBI also launched UPI for feature phones, which has the potential to attract 400 million users from rural and remote areas.

Zero MDR

MDR plays a crucial role in any company’s decision regarding choosing a payment gateway service provider. MDR is a fee or percentage a merchant has to pay to the payment gateway provider.

Typically, the fee is around 1.8% for most payment methods like cards and wallets. However, the MDR for UPI is zero, meaning that if a customer purchases something worth Rs 100 via UPI, the merchant gets the amount without any deductions.

The Implication of Increased UPI Growth – The Use Cases

The ubiquitous UPI has altered how India makes real-time payments each day in recent years. The transition from a cash-based to a cashless convenience has expanded the digital payment ecosystem beyond the privileged and technologically savvy.

With the required push from the government, consumer-payment apps, and Fintech startups, payment technology has managed to bring its benefits to the general public.

Released in 2018, UPI 2.0 transformed payment technology into the ultimate digital transacting platform and brought newer use cases for numerous industries to light.

The features that led to this transformation are:

- With one-click payments, users only need to enter the UPI pin and approve the transaction.

- Improved UI/UX to encourage feature phone users to use USSD-enabled UPI.

- Improved integration with BBPS for a smoother flow.

- Increase the transaction value limits. Useful for larger transaction sizes, such as education and SMEs.

- Enable recurring mandates and the ability to cancel them for smooth and secure transactions.

- Create financial literacy and awareness to enjoy the benefits effectively.

Here are the few industry-specific use cases of UPI that are gaining popularity and driving digital transactions:

| S. No. | Industry | Use Case |

| 1. | Travel | One-time mandate feature has made it possible for users to book tickets, taxis, and hotel room travel scheduled for dates in the future. |

| 2. | Financial Institutions (FIs) | Creating a credit profile by analysing data from UPI transaction history and OD facility usage for offering credit facilities. |

| 3. | eCommerce | It can successfully replace the cash-on-delivery payment option by allowing merchants to collect funds digitally at the time of delivery of goods. |

| 4 | Non-Banking Financial Companies (NBFCs) & Micro Finance Institutions (MFIs) | Creating mandates for UPI-based collections can be incentivised, which can significantly reduce payment collection costs. |

| 5. | Subscription | Using UPI-based mandates for blocking amounts towards DTH bill payments, streaming media subscriptions, quarterly school/gym fees, and more. |

| 6 | Healthcare | Providing more context to patients by enabling the sharing of pathology reports and medical observations at the time of successful payment collection. |

| 7. | Corporates and SMEs | Digitising B2B transactions by sharing digital invoices for purchases, collection requests, and periodic reminders. |

| 8. | Micro merchants | Increasing the use of low-cost QR-based payment acceptance at small mom-and-pop shops via signed intent. |

UPI – The Rocketship for Innovation in the Digital Payments Sector

The primary reason for the widespread adoption of UPI can be attributed to its ease of use with a large population. Furthermore, it has an open protocol on which other innovations can be built, allowing for a significantly bigger and more useful network for financial payments than its competitors.

It can accelerate global payment technology innovation by doing what blockchain technology is supposed to do – removing intermediaries and increasing competition.

The Government of India’s strategies for digitising the financial sector and economy also promote digital payment transactions, which have rapidly grown over the last few years.

These initiatives are designed to make the digital payments ecosystem a critical component of the Digital India program.

Why is Paytm PG the Best for UPI Payments?

Given the growing popularity of this payment technology as a means of payment among users, businesses must consider offering this payment source on their websites and apps.

As part of the payment gateway, Paytm also provides UPI payment solutions. Numerous businesses rely on our service for the reasons listed below:

- We have designed simple UPI flows that provide frictionless payment experiences.

- We empower businesses to accept payments via their customers’ preferred UPI method – UPI ID, UPI apps, or UPI-linked bank accounts.

- We have industry-leading UPI payment success rates.

- We offer 0% MDR charges on UPI payments and provide businesses with access to Paytm’s massive customer base.

In this blog, we have gone into great detail about what makes Paytm’s UPI solutions the best.