RuPay, the brainchild of the National Payments Corporation of India (NPCI), is a native card payments network launched by the Reserve Bank of India (RBI). This financial and payment system was unveiled in 2012 and dedicated to the country in 2014.

The term RuPay was coined by combining the words rupee and payment. The intention was to introduce India to the global payments market through its indigenous card facility.

RuPay’s Growth Story

Since its inception, RuPay has amassed a sizable market share in the Indian card market. According to RBI’s data, RuPay’s market share had risen to more than 60% of total cards issued as of November 30, 2020, up from 17% in 2017. However, RuPay controlled only 20% of the Indian credit card market.

As of November 2020, nearly 1,158 banks had issued approximately 603.6 million RuPay cards. However, a big part of this share included debit cards, with only 970,000 being credit cards.

According to a new RBI report, as of the end of January 2022, over 651 million RuPay debit cards were issued in the country. It accounts for more than 65% of the total debit cards issued. On the other hand, RuPay cards account for less than 3% of the credit card market in India.

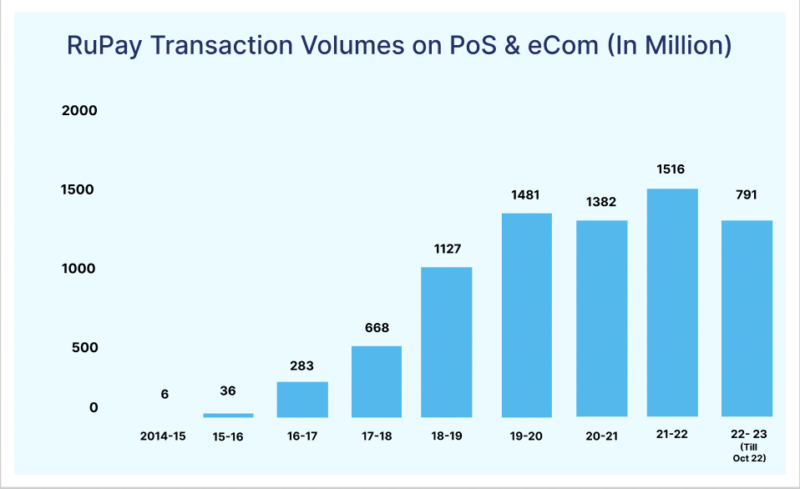

RuPay Transaction Volumes Over the Years

Source: GoI

Source: GoI

The transaction volumes, including point-of-sale transactions and eCommerce, have seen massive growth since its inception. The transaction volumes saw a 500% increase in FY 2015-16 compared to the previous year.

This table shows the year-on-year % changes in the transaction volumes of RuPay cards:

| Financial Year | RuPay Transaction Volume | YoY % Change |

| 2015-2016 | 36 million | +500% |

| 2016-2017 | 283 million | +686% |

| 2017-2018 | 668 million | +136% |

| 2018-2019 | 1,127 million | +69% |

| 2019-2020 | 1,481 million | +31% |

| 2020-2021 | 1,382 million | -7% |

| 2021-2022 | 1,516 million | +10% |

The transaction volumes have definitely increased at an impressive rate since its inception. The factors that have played a vital role in the increased adoption of this indigenous card-based payment solution are discussed in the next section.

Also Read: Growth of UPI Ecosystem: A Homegrown Technology Ready to Conquer the World

Factors that Contributed to the Rise of Rupay

Let us understand the factors that have contributed to this growth:

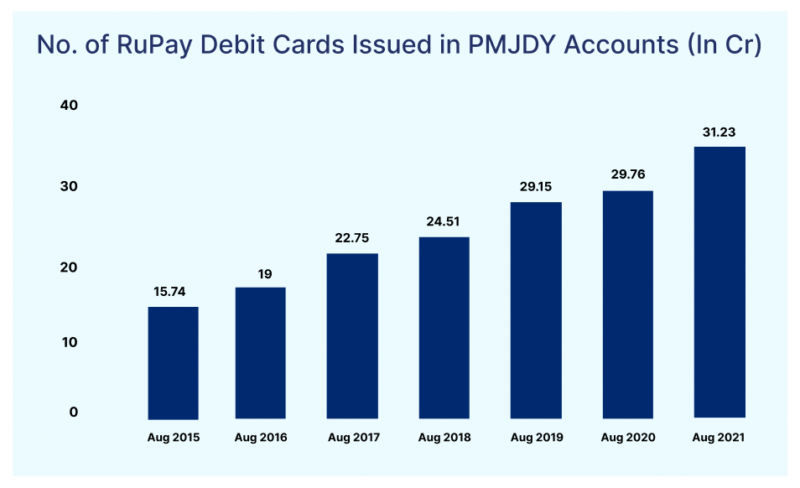

1. The focus on financial inclusion in the country has increased

In 2011, nearly half of the Indian population (557 million) did not have a bank account due to a high minimum balance requirement of 3-5k. This requirement was unaffordable for the unorganised sector. To address this, the government introduced the Jan Dhan Yojana in 2014, under which the government issued RuPay debit cards to new account holders.

As of December 2021, 44.23 crore bank accounts had been opened, with 31 crore Rupay debit cards issued through PMJDY. This scheme gave a significant push for RuPay to reach India’s unbanked population.

Source: Ministry of Finance

Source: Ministry of Finance

2. Government assistance is readily available

According to Visa’s annual report, one of the threats to their operations is government mandates and/or regulatory requirements on international transaction processes. They may prevent them from competing with firms in different nations, including larger markets such as China, India, and Russia.

The RBI established NPCI as a ‘Not-for-Profit’ organisation to build a domestic payment and settlement system in India. With the government and RBI’s goal of increasing financial inclusion in a country like India, NPCI is the ideal tool for focusing on subsidised services.

It enables them to serve all people earlier excluded from traditional banking services. Along with this, the government reminded people about the free Personal Accident Health Insurance that comes with all cards issued, with a particular emphasis on RuPay.

The government has long promoted RuPay to develop the homegrown card network and has also connected its usage to nationalism and loyalty to the country.

3. Support from public sector banks is there

With the government’s involvement, all public sector banks (PSUs) now issue only RuPay cards to new customers. According to reports, the government has requested PSU banks to offer far more RuPay cards to customers.

“RuPay card would have to be the only card you promote,” Finance Minister Nirmala Sitharaman said in November 2020 at a bankers’ conference.

Whoever needs a card, RuPay will be the only card that any bank will have to offer. She also implied that as an Indian citizen, no one should use any other card network than RuPay.

4. The financial benefit of RuPay is undeniable

RuPay, like the Unified Payments Interface (UPI), is subject to the Indian government’s Zero-MDR policy, which means merchants do not have to pay fees for transactions on these networks.

Furthermore, when banks use RuPay, their operating costs are lower compared to the global networks. Banks that issue MasterCard and Visa cards must pay a quarterly fee to participate in their network.

However, because it is a domestic network, banks are not required to pay this fee, so no processing or transaction fees are passed on to customers.

5. Problems faced by MasterCard paved the way for RuPay

MasterCard suffered a significant setback in 2021, adding to the already intense competition in the Indian market.

The RBI, in a notification, barred the network from issuing new cards beginning July 22, 2021, a boon for both RuPay and, in particular, Visa.

MasterCard was found violating RBI’s instructions on the Storage of Payment System Data, which required system providers to ensure that all payment system data be stored solely in India. As a result, various banks had to switch to RuPay and Visa cards.

Also Read: How India Paid in 2022: An Annual Overview of Digital Payments

RuPay Goes Global

When PM Modi visited the Indian Heritage Centre in Singapore in 2018, he purchased a Madhu-Bani painting. And how did he make the purchase? He used an SBI RuPay card.

It was an indication that the payment gateway was going global. As of 2019, RuPay was used by citizens from 195 countries. PM Modi launched the payment gateway in Saudi Arabia a few months later.

Earlier this year, our Finance Minister, Nirmala Sitharaman, confirmed Singapore and the UAE’s acceptance of the RuPay payment mechanism.

India is in discussions with 30 different nations to make RuPay a viable payment option in their country. Bhutan and Nepal had previously agreed to accept RuPay.

This year an MoU was also signed between India and Lyra Network of France that aims to enable the acceptance of RuPay and UPI in their country.

As of the beginning of FY 2022-23, RuPay was accepted in over 200 countries at 42.4 million PoS locations and 1.90 million ATMs.

So yes, strong steps are being made by the government to globalise this indigenous payment method.

Why is it Important to Globalise RuPay?

Globalising will make payment easier for RuPay cardholders. This card’s transactions cost 23% less than competing card brands. They also have a shorter processing time and lower processing fees.

Thus, globalising this payment system will make life easier for Indian cardholders. Another feather in RuPay’s cap is that the RBI is very strict about data security.

These features will increase RuPay’s global leverage while encouraging healthy competition between card issuers and diversifying consumer card options.

It will act as a wake-up call for all cards that have previously been overcharged throughout the processing chain.

It will also alleviate the burden of purchasing foreign currency before travelling abroad and the inconveniences of money transfers. Also, it will help students and tourists overcome financial constraints when travelling abroad.

The Russia-Ukraine war provides a niche advantage. Visa and MasterCard have ceased operations in Russia, which has created an excellent opportunity for India to fill the void.

India is ready to assume an international monopoly in the current era that is experiencing an economic shift, coupled with the recession and global volatility.

Want to read more such interesting blogs?